What is an Investment Risk?

All investments have some form of risk associated with them, i.e., they all expose you to the chance you could lose money (either notionally or permanently). In this Fact Sheet we discuss seven of the more common types of investment risk.

The risk of permanent loss of capital

The permanent loss of capital is the risk that you might lose some or all of your original investment. This usually occurs if the price falls and you sell an investment for less than you paid for it.

If an investment isn’t performing as expected for an extended period, you might contemplate selling it, thus realising a loss. However, before doing so, you should consider whether the downturn is simply due to market conditions from which it may recover, or whether it is truly a permanent risk to your capital. Poor quality investments may experience a fall in value from which they never recover. In extreme cases, their value can fall to zero. Therefore, regularly reviewing performance is an important aspect of investing.

The risk of volatility

Investment volatility is the risk of the value of your investment moving up and down. With high quality investments, their values should generally move up over time, more than they go down.

Investments which are expected to produce higher long-term returns, such as shares, tend to experience higher levels of short-term volatility.

On the other hand, investments which are expected to generate lower long-term returns, such as bonds, usually experience less volatility in the short term.

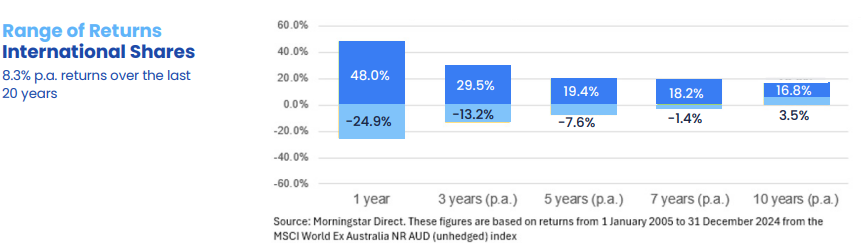

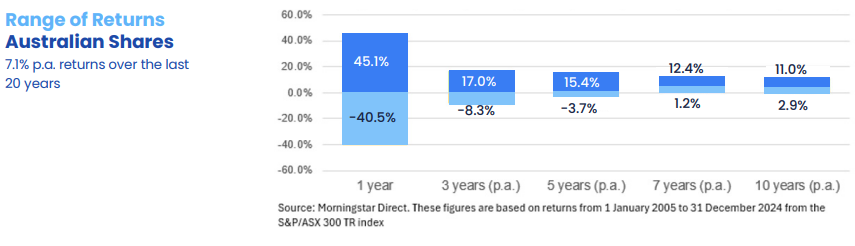

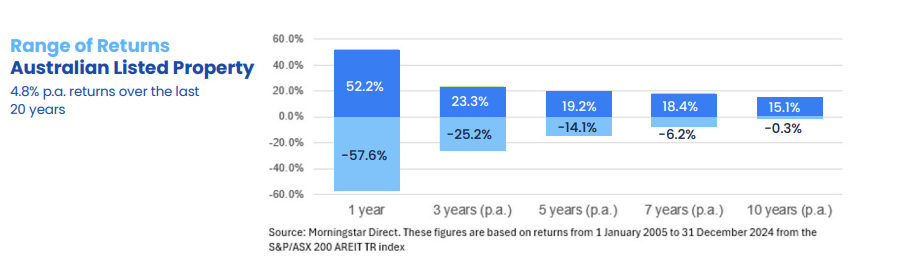

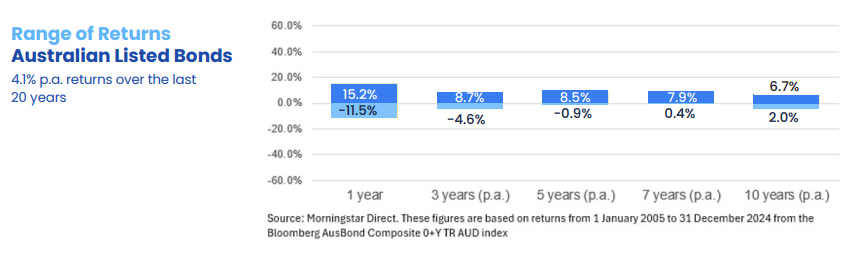

This can be seen in the charts below, which show the range of historical returns for various asset classes over various timeframes, as well as their historical returns over the last 20 years. As you can see, the longer you hold your investments the less they are affected by volatility. For example, the returns for Australian shares in any single year have ranged between -40.5% to 45.1%. However, the range over a 10- year period has been 2.9% to 11.0% p.a.

NOTE: Investors who redeem their investments after a fall in value turn a notional loss into a permanent loss. If they are high quality investments, this is usually a poor decision, because high quality investments generally recover from falls in value.

Wealth risk

This is where your investments don’t earn enough to help you achieve your financial or retirement goals.

This often happens if you choose safer investment options with lower returns and avoid options which have higher potential returns, but also a greater volatility. In such cases, you may need to lower your wealth or retirement expectations.

Credit risk

Credit risk usually applies to fixed interest investments. It refers to the possibility that the institution you’ve invested in might not be able to pay you the interest they promised, or return your original investment.

Inflation risk

This is where your money loses purchasing power because your investments do not keep pace with inflation. Cash is especially vulnerable to this risk because it often doesn’t earn enough interest to offset inflation.

Liquidity risk

Fixed term investments, or investments that have limited withdrawal windows, such as some hedge funds or property funds, expose you to liquidity risk. For example, if you need to access your money from fixed term investments before the term expires, you may be prevented from doing so under the contract. Or, if you can access your money, it might take longer than you want, and/or you may be charged significant penalty fees.

Poor quality share and property investments may also expose you to liquidity risk, as there may be no one who wants to buy them from you, or they will only buy them at a substantial discount.

Currency risk

When you invest overseas, your money is usually converted to the currency of the country in which you invest.

If the Australian dollar strengthens (rises in value) compared to the foreign currency, your investment will be worth less to you.

Conversely, if our dollar weakens (falls in value) against the foreign currency, your investment will be worth more.

To manage this risk, some fund managers use a strategy called hedging. Hedging aims to protect your investment from movement in the value of either currency.

How can you manage investment risk?

Investment risk can be managed using three prudent principles of investing:

Only invest in high quality investments

Construct a properly diversified portfolio

Regularly review your investments to ensure they continue to maintain their quality

Your Vision Financial Solutions Pty Ltd ABN 64 650 296 478 and its Advisers are Authorised Representatives of Fortnum Private Wealth Ltd ABN 54 139 889 535 AFSL 357306. This article has been prepared without taking into account your personal objectives, financial situation or needs.