Changes to the taxation of investments: Understanding the 2026 Federal Budget proposals

The 2026 Federal Budget proposed changes to how some investments may be taxed.

This article explains the key tax announcements and what they could mean for you.

What are the proposed changes?

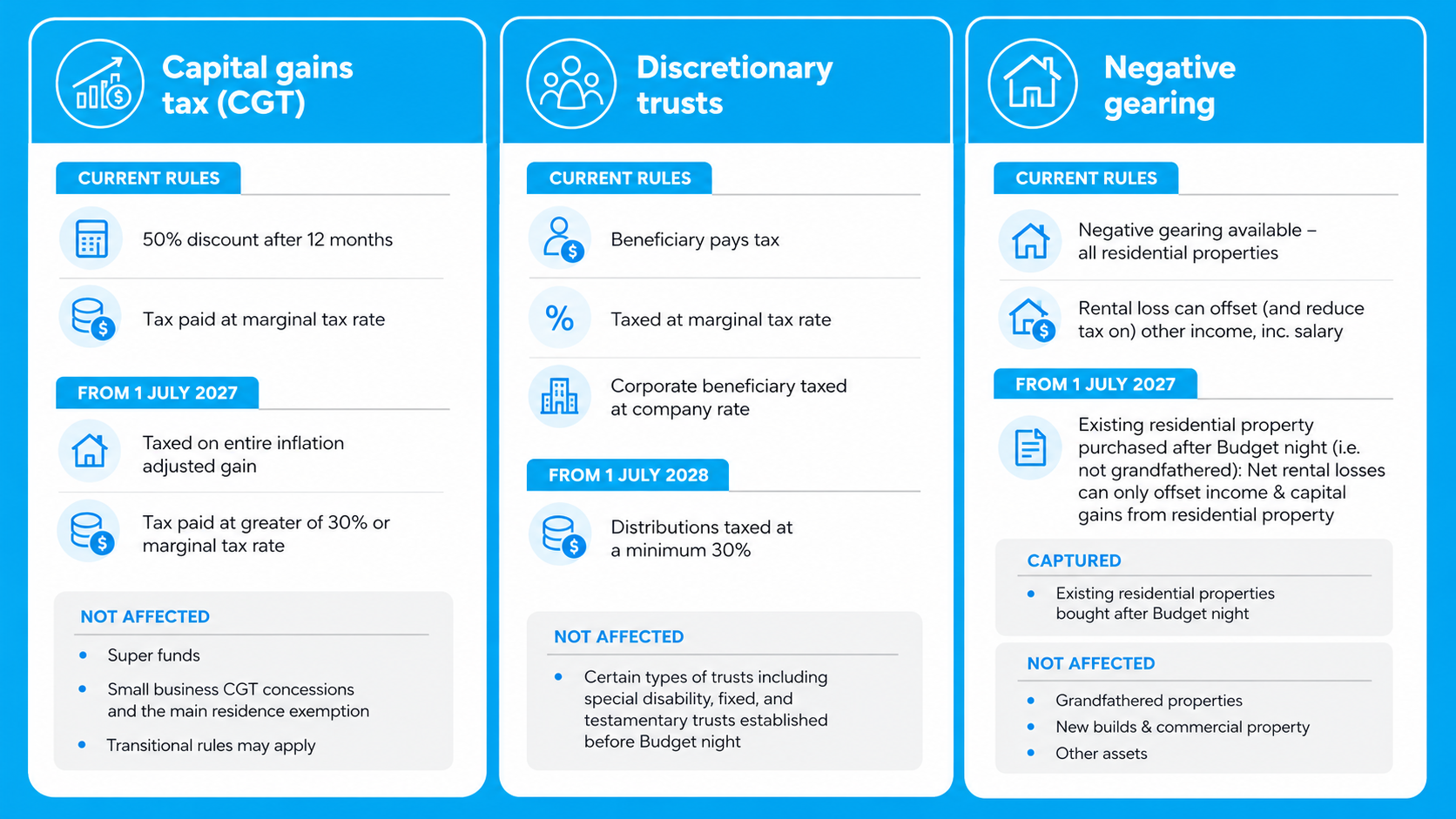

The 2026 Federal Budget has introduced significant tax proposals and if made law, they could impact your financial planning strategies. The key tax proposals include changes to Capital Gains Tax (CGT), negative gearing for residential property, and the taxation of discretionary trusts.

While the announcements are only proposals, it’s important to understand their potential implications for your investments and financial strategies.

This guide aims to demystify the announced changes. We will explore the measures, the potential effects, and common questions you might have, to help you navigate this evolving landscape with confidence. We recommend seeking personalised advice from a financial adviser to understand how they specifically apply to your unique circumstances.

Capital Gains Tax (CGT) changes

INDIVIDUALS | TRUSTS | PARTNERSHIPS | SMALL-BUSINESS OWNERS

From 1 July 2027

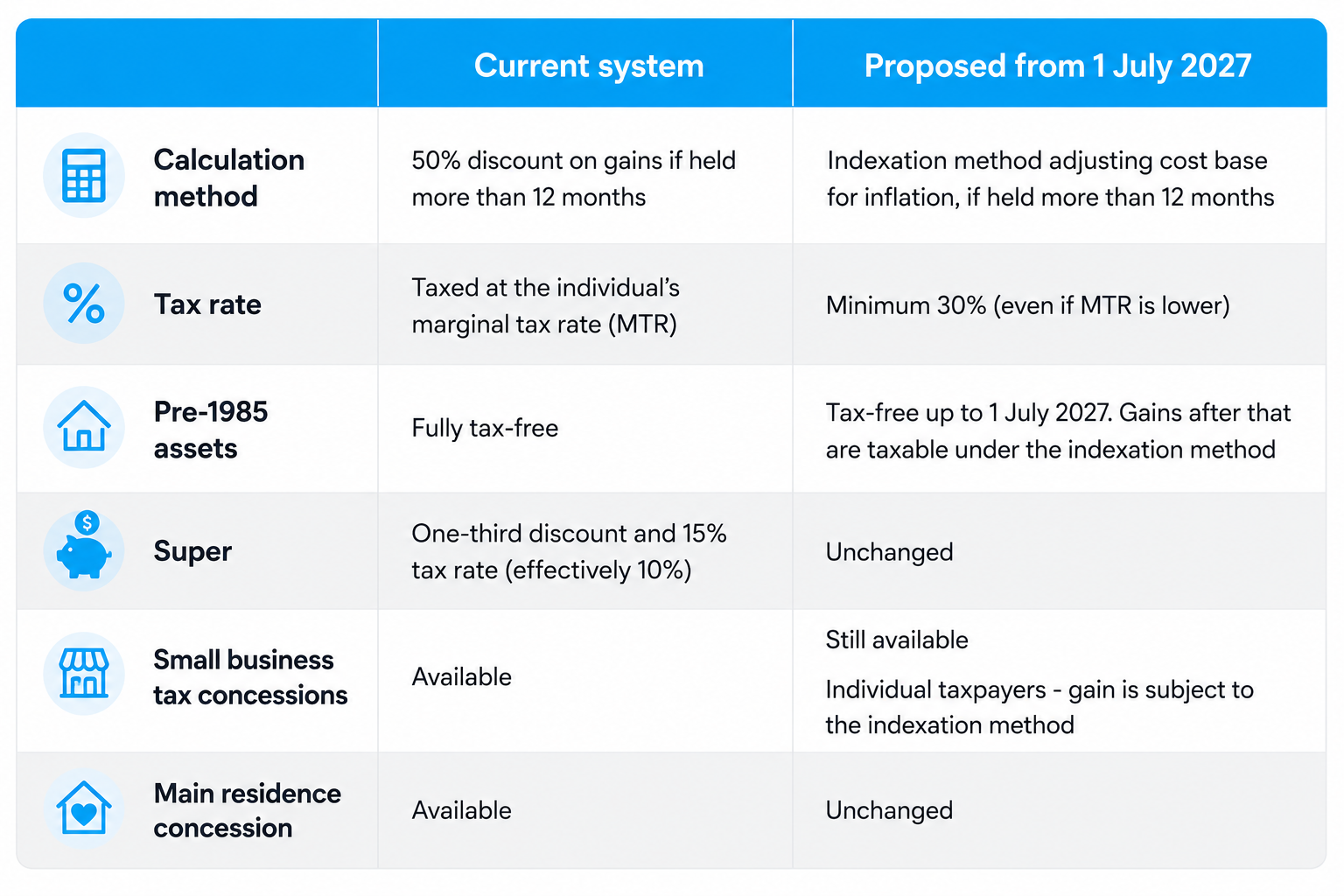

Capital gains accrued from 1 July 2027 will not be eligible for the existing 50% CGT discount. Instead, the discount will be replaced with an ‘indexation-based’ approach. Under this method, the starting value of the asset for tax purposes is adjusted for inflation before tax is calculated. This means tax generally applies to the real gain – that is the return you’ve made on your investment above inflation.

A minimum 30% tax rate will also apply to capital gains from the same date, with limited exceptions.

Investors in eligible new residential properties can choose between the 50% CGT discount and the alternative method using indexation subject to the minimum 30% tax.

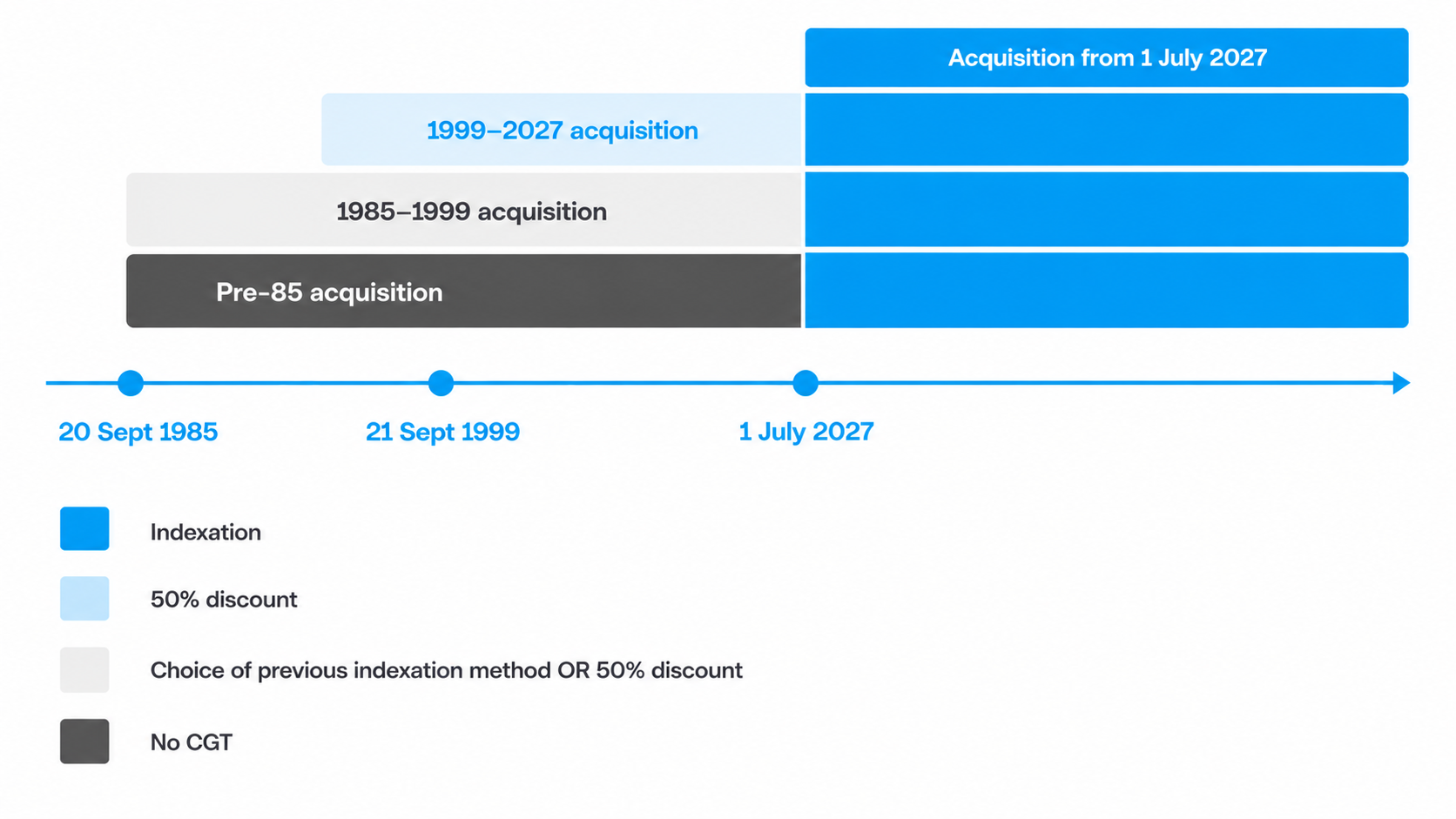

Chart: How CGT for a period is determined based on when the asset was acquired, and how long it’s owned for

Common questions and answers

Q1: How do these CGT changes apply to different types of investments?

The CGT changes would apply broadly across most asset classes. This means these are not limited to real property and may affect:

share portfolios

managed fund investments

business assets

most other non-super investments held by individuals or trusts.

Q2: When do these CGT changes take effect, and what is the significance of 1 July 2027?

The proposed start date for these changes is 1 July 2027. For assets you already own, a valuation as at 1 July 2027 may be crucial. This valuation will help distinguish the growth that occurred before the changes, which may remain eligible for the 50% discount, from the growth that occurs after, which is subject to indexation. You may be able to determine this value by:

market data

obtaining a formal valuation, or

using an apportionment formula provided by the ATO.

The most appropriate valuation approach can vary depending on the type of asset. For example, a listed share could be valued based on the closing market price on 30 June 2027. However, it may be more appropriate to have a formal valuation for an investment property.

Q3: How are my existing assets impacted?

Under the proposed changes, if you sell an asset after 1 July 2027 that you acquired before this date, the capital gain will be calculated in two parts:

Gains accrued up to 30 June 2027: These gains will still benefit from the current 50% CGT discount (if held for at least 12 months). This means only half of the gain accrued during this period will be subject to tax at your marginal tax rate.

Gains accrued from 1 July 2027 onwards: For this portion of the gain, the asset's cost base will be adjusted for inflation. The indexed gain will then be taxed at your marginal tax rate, taxing the real gain after accounting for inflation. This is subject to a minimum tax rate of 30%. This means if your marginal tax rate is higher than 30% then you will pay that rate. However, if your marginal tax rate is lower than 30%, the gain

is subject to tax at this minimum rate.

For assets acquired on or after 1 July 2027, the indexation method will apply to the entire gain.

Q4: I own assets acquired before 20 September 1985 (pre-CGT assets). How will these be treated?

Gains on assets acquired before 20 September 1985 are entirely tax-free. Under the proposals, this tax-free status would partially end:

Gains accrued up to 1 July 2027: These gains will remain exempt from CGT, preserving the original pre-CGT benefit.

Gains accrued from 1 July 2027 onwards: These gains would become taxable under the new indexation method. The market value of your pre-CGT asset as at 1 July 2027 would effectively become its new cost base for calculating future taxable gains.

Q5: Does indexation affect both capital gains and losses?

No. The indexation method is used when determining the taxable capital gain (the sale amount less the indexed cost base). Indexation is not applied to the cost base when determining the size of a capital loss.

Q6: What is the new minimum 30% tax on personal capital gains?

From 1 July 2027, personal net capital gains will be subject to a minimum tax rate of 30%. This means:

If your MTR is higher than 30%, your capital gains would continue to be taxed at your higher MTR.

If your MTR is lower than 30%, your capital gains would be taxed at 30% instead of your lower MTR.

In effect, 30% becomes a minimum or floor for the tax rate on capital gains. This would mainly affect low to middle-income investors and retirees who previously paid little or no tax on capital gains due to the 50% discount and their lower marginal tax rates.

Case study: Impact of the 30% minimum tax

May is a retiree with low taxable income. She sells investments in 2027/28, releasing a $100,000 capital gain.

Under the current system: May could apply the 50% CGT discount, reducing her taxable gain to $50,000. This amount would taxed at her MTR, resulting in tax of approximately $7,252.

Under the proposed system (from 1 July 2027): Assuming the entire gain is subject to the new rules, May’s $100,000 gain is adjusted for indexation so that she’s only taxed on the real growth in the value of the property, not the amount that’s due to inflation. She’s subject to the minimum 30% tax rate on the entire gain. Let’s assume for simplicity that after adjusting the cost base of the property for inflation, the real capital gain is $85,000. She’d pay tax at 30% on this entire amount, resulting in tax of approximately $25,500.

Note: This is a simplified example ignoring income from other sources . Actual calculations will depend on indexation rates and the specific timing of asset acquisition and sale.

What this shows: These changes may matter most if you are on a lower tax rate, are nearing retirement, or expect to rely on selling assets to help fund your lifestyle.

Q7: Are there any exemptions from the 30% minimum CGT tax rate?

Yes. The Government has indicated that individuals receiving certain means-tested social security payments in the financial year the gain is realised, such as the Age Pension, Disability Support Pension, Carer Payment and JobSeeker, are exempt from the 30% minimum tax. This is intended to protect vulnerable or lower-income individuals who rely on these benefits.

Q8: How do these changes affect investments within super?

The CGT rules for super funds, including self-managed super funds (SMSFs) remain unchanged under these proposals:

Super funds will continue to benefit from their one-third CGT discount for assets held for more than 12 months. The indexation rules do not apply to super funds.

Investment earnings in super remain taxed at up to 15%, or effectively 10% on discounted capital gains, and may be 0% in pension phase. The new 30% minimum tax rate on capital gains does not apply to super funds.

This means the relative tax advantage of holding growth assets within super may become more significant compared with holding these personally from 1 July 2027.

Q9: What about main residence and small business CGT concessions? Are they impacted?

No. These concessions remain unchanged.

Q10: Can I still use strategies like deductible super contributions to reduce my CGT?

While concessional super contributions, other personal tax deductions and some tax offsets may still help reduce your overall taxable income or total tax bill, these are unlikely to reduce the tax payable on your net capital gains below the proposed 30% minimum. This is because the measure is intended to apply specifically to net capital gains, effectively ring-fencing them from the usual benefit of lower marginal tax rates. In practice, strategies that may still matter are likely to include using available capital losses, carefully timing asset sales, making sure any available exemptions or concessions are claimed, and considering whether the ownership structure remains appropriate. For example, superannuation continues to operate under different tax rules, so for some people it may still offer a more concessional environment for future growth assets.

Negative gearing changes

RESIDENTIAL PROPERTY INVESTORS | INDIVIDUALS | TRUSTS | PARTNERSHIPS | COMPANIES

From 1 July 2027

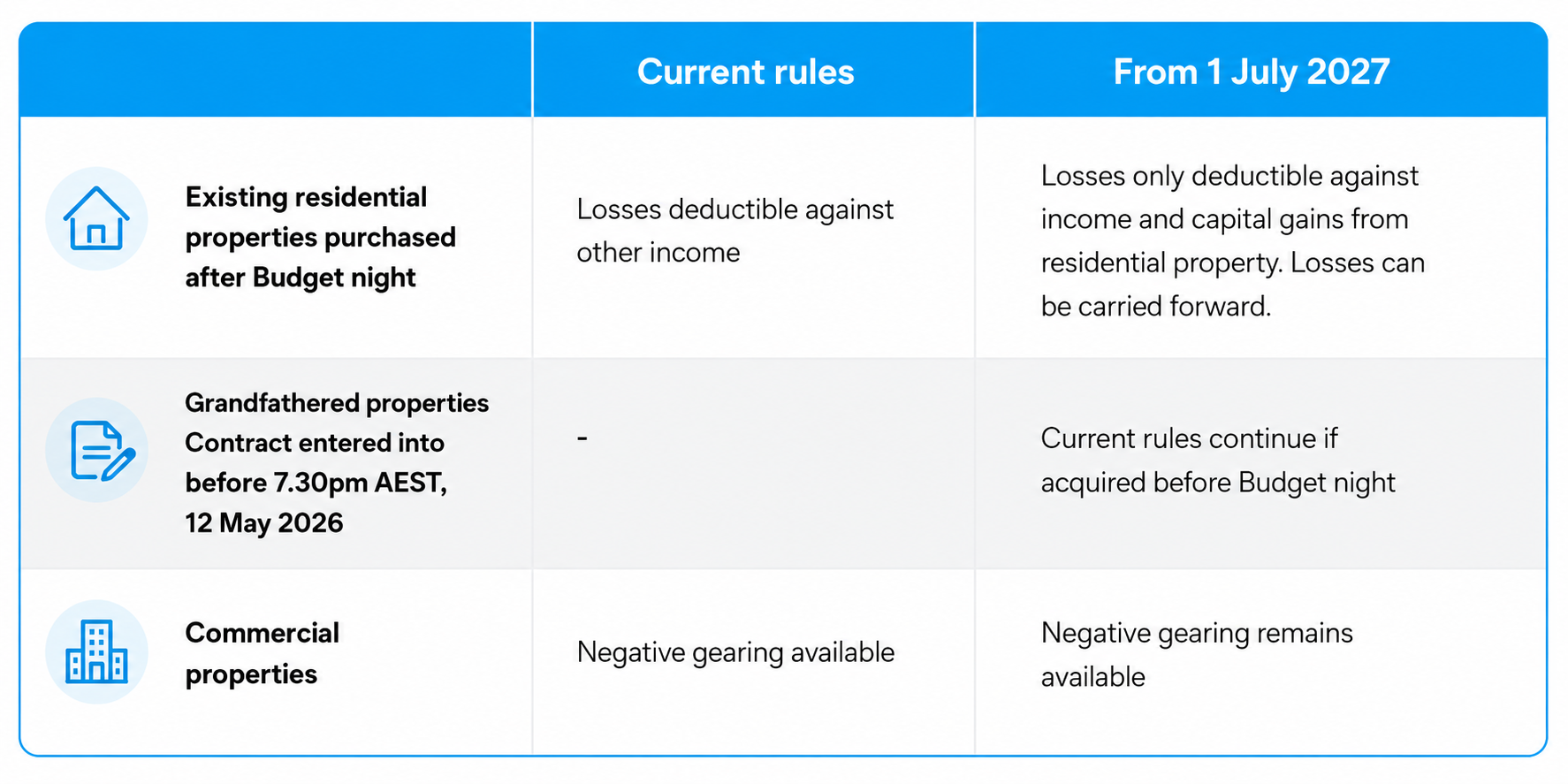

The Government proposes to limit negative gearing tax benefits (on residential property) to new housing. This means that for existing residential properties purchased after 7.30pm Australian Eastern Standard Time (AEST), 12th May 2026 (Budget night), net rental losses will no longer be deductible against other income.

Case study: negative gearing for residential properties

Mark purchases an existing investment property on 1 June 2026. In the 2027/28 financial year, his property incurs a net rental loss of $10,000.

Under the current system: Mark could use the $10,000 net rental loss to reduce his taxable income from other sources, such as salary, potentially saving tax in that year

Under the proposed system (from 1 July 2027): Mark purchased the property after Budget night, so while he can negatively gear the property between now and 30 June 2027, he’s not eligible for negative gearing from 1 July 2027. He can’t use the $10,000 loss to reduce salary or other non-residential property investment income from 2027/28 onwards. Instead, the loss can be carried forward and can be used to offset future positive rental income from residential properties or to reduce the capital gain when the property is sold.

If on the other hand, Mark had purchased the existing residential property before Budget night, or the property was an eligible new property, he wouldn’t be impacted by the new rules.

What this shows: The proposed rules may reduce the upfront tax benefits of buying existing residential property, which means cash flow and long-term investment fundamentals may become even more important. This example highlights the cash flow impact of the changes, as the immediate tax benefit is reduced.

Common questions and answers

Q11: What exactly is changing with negative gearing?

Currently, if your investment property expenses, such as interest on your loan, rates and maintenance, are more than the rental income it generates, you can use that net rental loss to reduce your taxable income from other sources, such as your salary. This is known as negative gearing.

The proposed changes, effective from 1 July 2027 , will restrict this benefit to:

New builds: If you buy a newly built residential property, or create new dwellings, such as building on vacant land, you can continue to negatively gear by offsetting rental losses against other income.

Existing properties: For existing residential properties purchased after 7:30 pm AEST on 12 May 2026, net rental losses can no longer be deducted against other income. They can only be used against income and capital gains from residential property, and losses can be carried forward to reduce future residential property income. An exception may exist if changes are made that classify it as a ‘new build’ - see Q16.

Q12: Which types of property are affected by these changes?

Negative gearing changes apply specifically to residential property investments . Commercial properties, such as offices, industrial warehouses or retail spaces, are not affected.

Q13: When do these negative gearing changes apply, and what does grandfathering mean?

The changes are proposed to begin on 1 July 2027. Here is how the timing and grandfathering rules are proposed to work:

Grandfathered properties: If you owned a residential investment property, or had entered into a contract to buy one, before 7:30 pm AEST on 12 May 2026 (Budget night), your property is grandfathered and can continue under the current negative gearing rules.

Existing residential property purchased after Budget night: If you enter a contract after Budget night and before 1 July 2027, you can still negatively gear the property until 30 June 2027. From 1 July 2027 onwards, losses are quarantined and can only be offset against income and capital gains on residential property, not salary or other non-property income.

An exception may exist if changes are made to the property to classify it as a ‘new build’ - see Q16.

Q14: What happens to rental losses that I can no longer offset against my other income?

If your rental losses are quarantined, they are not lost. They are carried forward to future years and can generally be used in two ways:

Offset against future rental income: Carried-forward losses can reduce future positive rental income from residential investment properties.

Reduce capital gains on sale: If you sell the property, accumulated losses can reduce the capital gain and therefore lower the CGT payable at the point of sale. We will need to wait for the legislation before the calculation is fully clear.

Q15: Can losses from one residential property be offset against income from another?

Yes. Current guidance suggests quarantined losses can generally be applied across your residential property portfolio. This means losses from one residential property may be used to reduce net rental income from another, but not commercial property and non-property income (such as salary).

Q16: What qualifies as a new build for continued negative gearing benefits?

For residential property to qualify as a new build and retain full negative gearing benefits, the property must contribute to new housing stock . Examples include:

buying a brand new dwelling directly from a developer.

building a new house on vacant land, and

significantly redeveloping an existing property to create additional dwellings, such as converting a single house into a duplex or multiple units.

Simply renovating an existing property or adding a minor dwelling, such as a granny flat, generally won’t qualify as a new build. The key test is whether the investment genuinely increases overall housing supply.

Q17: Should I still consider investing in residential property given these changes?

Investment decisions should always be based on your goals, risk tolerance and overall strategy. While the tax benefits of negative gearing for existing properties may change, reducing the upfront and ongoing tax concessions, property investment may still offer capital growth and rental income. A financial adviser can help you assess the long-term investment fundamentals along with the impact on the loss of immediate tax deductions.

Discretionary trusts changes

BENEFICIARIES | TRUSTEES | INDIVIDUALS | SMALL-BUSINESS OWNERS | COMPANIES

From 1 July 2028

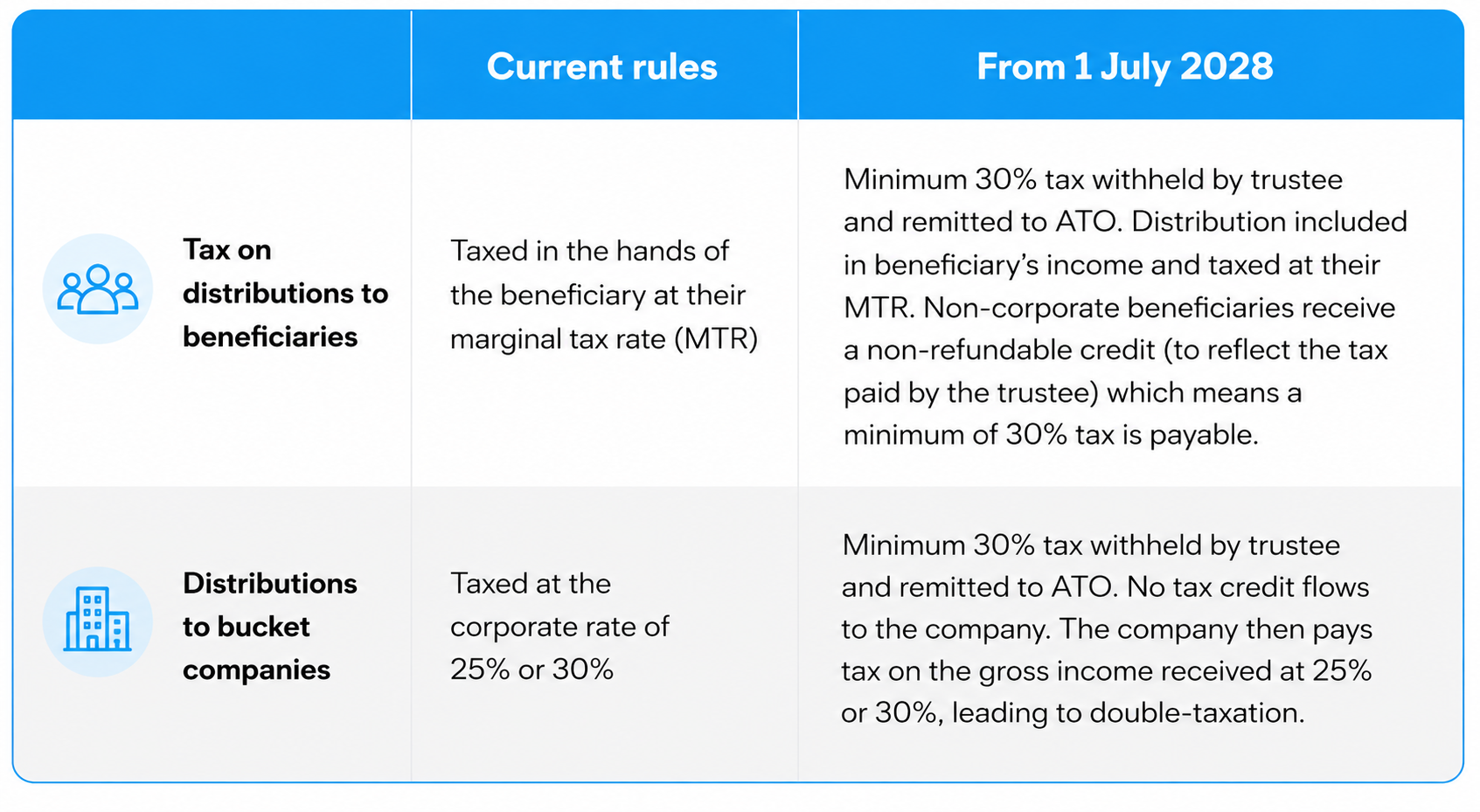

Discretionary trusts will be subject to a minimum 30% tax on distributions (unless a higher rate of tax would apply). This is intended to reduce the tax advantages of distributing trust income to beneficiaries on lower MTRs and may particularly affect income-splitting and bucket company strategies.

Q18: How will the new tax be applied, and how do the credits work?

The trustee will be responsible for withholding tax at 30% on all distributions and remitting this to the ATO. Individual beneficiaries will receive a non-refundable tax credit to recognise the tax that has already been collected (to make sure there’s no double taxation). If the beneficiary’s MTR is higher than 30%, they may need to pay more tax (after allowing for the 30% withheld). If it is lower than 30%, they will not receive a refund for the difference. In effect, this sets a 30% floor on the tax outcome for these distributions. The minimum tax will not apply to certain income, such as primary production income and certain income to vulnerable minors.

Q19: Which types of trusts are affected by this new tax?

This new tax is primarily aimed at discretionary trusts , including many family trusts. Some trusts are expected to remain outside the new rules, including:

fixed or unit trusts

widely held trusts, such as public unit trusts or managed funds

charitable trusts

special disability trusts, and

testamentary trusts created before 7.30pm, AEST, 12 May 2026 (Budget night). Discretionary (not fixed) testamentary trusts created after Budget night are proposed to fall under the new rules.

Q20: How will distributions to bucket companies be affected?

The common strategy of distributing trust income to a bucket company is expected to be significantly affected. Under the proposed rules:

the trust would first pay 30% tax on the distribution to the bucket company,

the bucket company is taxed again on the income at its corporate tax rate, and

the bucket company does not receive a credit for the 30% tax paid by the trust.

This could produce a much higher overall tax outcome and significantly reduce the tax benefits of using a bucket company to cap the tax rate on trust income. Existing trust distribution strategies may need review before 1 July 2028. Rollover relief (including capital gains tax) is available for three years from 1 July 2027 to assist small businesses and others to restructure out of a discretionary trust into another type of entity (eg company or fixed trust).

Case study: Discretionary trusts and bucket companies

A discretionary trust distributes $100,000 of income to a bucket company in the 2028/29 financial year. The bucket company’s tax rate is 25%.

Under the current system: The trust distributes $100,000 to the company. The company pays 25% tax, resulting in a tax bill of $25,000. The remaining amount may then be retained and invested, or later paid as franked dividends to shareholders.

From 1 July 2028: The trust first withholds 30% ($30,000) tax on the $100,000 distribution. The company receives the remaining $70,000 and does not receive a credit for the $30,000 tax paid by the trust. The company then pays 25% tax on the $100,000, resulting in additional tax of $25,000. The total tax paid on the $100,000 income is $55,000, significantly increasing the overall tax burden compared with the current system, and reducing the effectiveness of the bucket company strategy.

What this shows: Trust strategies that currently work well for tax planning may become less effective, particularly where income is being directed to a bucket company or lower-tax beneficiaries

Q21: Are bucket companies being banned?

No. There is no indication that bucket companies are being banned. However, their effectiveness as a tax planning tool is expected to be significantly reduced as explained above, which means existing structures may need to be reviewed for ongoing suitability.

Q22: What happens to franking credits on dividends received by a trust under the new rules?

The policy intent appears to prevent trusts from using franking credits to manage the 30% minimum tax to beneficiaries. It is expected that franking credits attached to dividends received by a discretionary trust are first applied against the minimum tax rather than flowing through to beneficiaries, although the final legislative detail will confirm the exact treatment.

In other words, if those franking credits were allowed to flow through to the final beneficiary, they could reduce that beneficiary’s personal tax. That would effectively undermine the policy intent by creating a way around the new 30% minimum tax.

Q23: Will discretionary trusts still need to distribute all their income annually?

It is not a requirement for a trustee to distribute all income annually either today or under the proposed changes. However, trustees generally distribute all income each year to avoid the trustee being taxed at the top marginal tax rate (MTR), exceptions apply. While the structure continues to operate, the proposed 30% minimum tax reduces the flexibility and tax benefit of distributing income to lower-rate beneficiaries.

Q24: Is there any relief for small businesses to restructure due to these trust changes?

Yes. The Government has proposed a small business restructuring relief, expected to apply from 1 July 2027 to 30 June 2030. This may allow qualifying businesses to move from a trust to a company structure without triggering immediate CGT consequences. This three-year window is intended to help business owners transition away from structures affected by the new trust tax, although state taxes such as stamp duty may still need to be considered.

Before restructuring, some considerations may include:

Asset protection: whether the structure helps protect business or family assets.

Flexibility: how easily income can be distributed or retained.

Succession and estate planning: how the structure fits with longer-term family and business plans.

Access to concessions: whether a change could affect eligibility for tax or small business concessions.

Financing and commercial requirements: whether lenders, investors or other stakeholders have preferences around structure.

Transfer costs: whether moving assets or business operations could trigger stamp duty, tax or other costs.

What should I consider if I think that these proposals could impact me?

Navigating changes to tax legislation can be complex. If you think these proposals may affect you, it’s worth discussing the possible implications with a financial adviser. While this guide provides a general overview, your personal circumstances will shape the strategies most relevant to you. Some key areas to consider with an adviser include:

For CGT changes

Reviewing your investment portfolio: Identify which assets, such as shares, managed funds and investment properties, may be affected by the shift from the 50% discount to indexation, as well as the new 30% minimum tax.

Record-keeping and valuations: Given the importance of the 1 July 2027 valuation date, consider what records you need to maintain and whether formal valuations for some assets may be worthwhile.

Impact on retirement planning: Consider how the 30% minimum CGT rate may affect your income strategy if you expect to rely on asset sales, especially if you are nearing or in retirement.

Use of capital losses: Consider whether any existing or future capital losses could help reduce taxable gains.

Ownership structure: Consider whether holding future growth assets personally, jointly, in a trust or company, or through super remains the most appropriate approach.

For negative gearing changes

Assessment of existing and future property investments: Confirm whether your current residential investment properties is grandfathered (ie exempt from the changes). If you are considering new property investments, compare the implications of new builds versus existing properties.

Cash flow management: If you own existing properties purchased after Budget night that may no longer offset losses against other income, think through the possible impact on your cash flow.

Long-term investment strategy: Revisit your broader property strategy in light of the proposed changes, including how deferred losses may be used and the overall return profile of your investments.

Debt and funding strategy: Review whether your loan structure and repayment strategy remain appropriate if losses can no longer reduce salary income.

Portfolio mix: Consider whether the balance between residential property, commercial property and other investments still suits your goals.

For discretionary trusts changes

Review of trust distribution strategies: If you use a discretionary trust, review how the 30% minimum tax could affect distributions to lower-rate beneficiaries and bucket companies.

Potential restructuring: Consider whether the proposed small business restructuring relief may be relevant and whether an alternative structure, such as a company, may better suit your objectives.

Estate planning implications: Consider whether the proposed changes could affect your broader estate planning objectives and the intergenerational transfer of wealth through your trust.

Cash flow impact: Consider whether the trustee or beneficiaries may need to fund additional tax earlier than under the current rules.

Trust deed and legal review: Consider whether the trust deed and legal structure provide enough flexibility if the rules change.

No immediate action may be needed yet: As these measures are still proposals, it is important to monitor developments to understand any concessions that become available and the appropriateness to your circumstances.

Questions to ask your adviser

These proposals highlight how quickly the financial planning landscape can evolve. Proactive engagement with your financial adviser can help you understand the possible implications, adapt your strategies and make informed decisions if the measures proceed. Some questions to ask are:

Could these proposals affect the way I hold future investments?

Should I review any property purchases, planned asset sales or trust arrangements?

Do I need valuations, better records or updated advice before the proposed start dates?

Is there anything I should do now, or is it better to wait for further detail?

Where to from here?

The proposed changes to CGT, negative gearing and discretionary trusts represent significant potential shifts in the Australian tax landscape. While these measures remain proposals and are subject to the legislative process, understanding their possible impact is an important part of effective financial planning.

We strongly encourage you to discuss these proposals with your financial adviser. They can provide tailored advice, help you assess how the changes may affect your personal circumstances and investment strategies, and guide you through any adjustments that may be needed.

Sources:

MLC, Changes to the taxation of investments, May 2026

Your Vision Financial Solutions Pty Ltd ABN 64 650 296 478 and its Advisers are Authorised Representatives of Fortnum Private Wealth Ltd ABN 54 139 889 535 AFSL 357306. This article has been prepared without taking into account your personal objectives, financial situation or needs.